Smart contracts provide plenty of benefits, but find out why those benefits can be just one side of a double-edged sword.

When was the last time you got a late payment? Chased an invoice? Waited for your monthly paycheck only to realize it’s late yet again? You might relate to these headaches as an investor, employee or client. But the tension that affects each of these unique parties is often caused by one unwavering contributor: an underlying traditional contract.

Contracts affect every organization’s workforce, and 26% of employees are involved in managing these agreements at some point, according to the World Commerce and Contracting Association. With such a vast effect on a company’s contributors, these contracts should be up to par with the rest of a business’s advancements. Unfortunately, contracts are still typically left to human maintenance and execution by either involved party, which can lead to some pretty costly oversight and error.

Blockchain-based smart contracts can revamp businesses and stakeholder relationships but, as with most major structural changes to a company, it’s important to do them right.

Work smarter, not harder

The current style of contracts is flawed and antiquated, but organizations have done little to change that. Poor contract management typically costs companies at least 9% of their bottom line, a consistent value leakage that can even reach a 40% loss, according to PwC. This revenue loss comes from incorrect data entry, unpaid accounts, client-management issues, incorrect reporting and discounting — essentially all caused by human error.

And the mishaps don’t stop there. Miscommunications and unmet contract terms can occur simply because an involved party is not on top of the predetermined agreements. This creates a whole slew of complications, like friction between companies and their employees or external partners that is often left to legal experts to address. A contract should provide clarity and reliability, not raise questions that require even more time and energy to address.

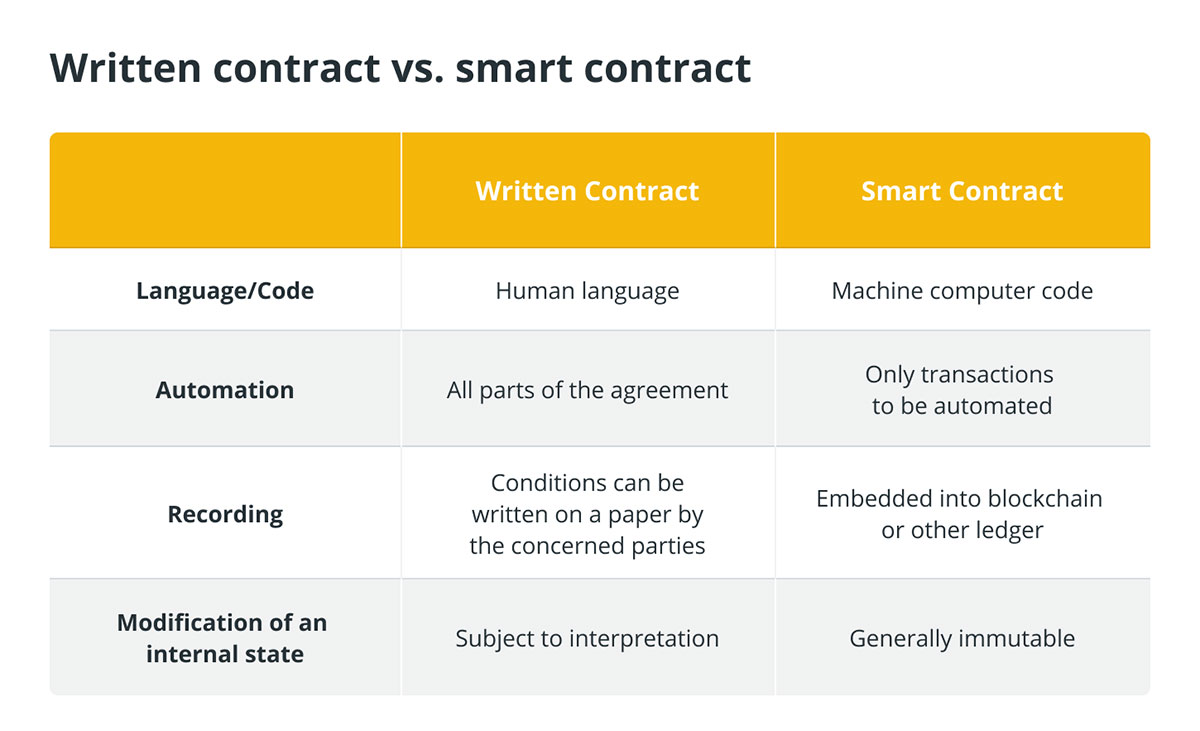

Companies can proactively prevent these issues from arising by bringing their contracts up to speed with the rest of their innovation. Smart contracts are stored on the blockchain and, unlike traditional contracts, are executed by the blockchain’s programming rather than by a person. So, smart contracts can enforce the terms of legal contracts automatically. This relieves either party from remembering the agreement and timelines, ensuring simplified and definite term executions.

Smart contracts don’t just mean that the contract itself is smarter, but that everyone involved is working smarter too. Without the need to manage and meet terms, people can focus on their actual jobs, making for a more efficient and productive workforce. Employees, clients, vendors, and other parties on the receiving end of a payroll don’t have to chase down a company for compensation. And people can trust unbiased code over an employer or business partner who could easily forget something or not have the other party’s best interest in mind. Read More at COINTELEGRTAPH![]()

Please Read Essential Disclaimer Information Here.

© 2024 Crypto Caster provides information. CryptoCaster.world does not provide investment advice. Do your research before taking a market position on the purchase of cryptocurrency and other asset classes. Past performance of any asset is not indicative of future results. All rights reserved.

Contribute to CryptoCaster℠ Via Metamask or favorite wallet. Send Coin/Token to Addresses Provided Below.

Thank you!

BTC – bc1qgdnd752esyl4jv6nhz3ypuzwa6wav9wuzaeg9g

ETH – 0x7D8D76E60bFF59c5295Aa1b39D651f6735D6413D

MATIC – 0x7D8D76E60bFF59c5295Aa1b39D651f6735D6413D

LITECOIN – ltc1qxsgp5fykl0007hnwgl93zr9vngwd2jxwlddvqt